As 2024 starts to come to a close, I want to spend some time talking about first-time homebuyers. Even if you already own a home, this is an important message to share; it can change someone’s life! In 2023, according to the National Association of Realtors (NAR) 2023 Profile of Home Buyers and Sellers, first-time home buyers represented 24% of the market share, which was down from 32% in 2022. First-time homebuyers are a critical part of the real estate market cycle, and we need to empower this group to invest in their future. They are also the audience that purchases inventory, enabling sellers to move on to their next home, which creates a domino effect as it travels up the market.

Often, first-time homebuyers purchase entry-level properties such as condos, townhomes, or smaller single-family residential homes based on affordability. It is also important to note that a buyer does not need a 20% down payment to purchase a home. In fact, according to NAR, the typical down payment for a first-time homebuyer in 2023 was 8%. There are loan programs that only require 3% down payments and even assistance programs requiring zero down. It is important to explore options so one knows their opportunity potential. For example, lenders will often advise borrowers to focus on saving vs. paying down debt in order to better qualify for a loan.

Sometimes, first-time homebuyers are able to skip that first level of home ownership and purchase a home that they plan to be in for many years, yet that is rare. I have found that it is critical that first-time homebuyers are focused on what monthly payment they feel comfortable taking on and commit to shopping at that price point. They then apply that price point to a combination of location, property type, and the condition/features they can afford.

The primary benefit of ditching the rent payment and becoming a first-time homebuyer is getting on the trajectory of building household wealth. As you can see from the charts below, real estate has appreciated in both King and Snohomish counties over the last 10 years, whether it be a condo or a single-family residential property. This appreciation becomes a nest egg of savings for the homeowner over time.

For example, if you use the data from the Snohomish County Condo chart, a first-time homebuyer who bought a condo in 2020, the median price in the market was $379,000. That is now $533,000, which is a 41% gain. Granted, these are raw numbers and represent a 30,000-foot view of the market, which illustrates the trends. We can’t simply apply the percentage growth in the market overall; we would analyze comparable properties in the specific area of the subject property to find the accurate value. The appreciation trend, however, shows that the first-time homebuyer who bought in 2020 is now sitting on a healthy nest egg of savings to utilize to purchase their next home if they desire a different property based on life changes. Plus, there is no other investment vehicle that allows tax-free capital gains up to $500,000.I point this out because I often encounter would-be first-time homebuyers who call off their search because they cannot afford the type of home or area they want, and continue to rent in the hopes of saving more to afford what they want later. While I would never want anyone to buy a home they don’t want, I do encourage my clients to consider what they can compromise on in order to start building wealth through homeownership sooner rather than later. Even if you apply the home appreciation for condos in Snohomish County prior to the pandemic, the median price in 2015 was $246,000, and four years later, it was $353,000, which is a 44% gain. Most people would not be able to save that much over that period of time, hence the advantage of building wealth via homeownership.

An exercise I often use with my buyer clients is applying the Triangle of Buyer Clarity to their budget and search. I am the first person to say that shopping for a home is exciting and even romantic, which results in starry eyes focused on dream homes and HGTV lore. I find that the quicker a buyer is able to put the dreaming part aside and get to the brass tacks of the market, the quicker they succeed in a purchase. Monthly payment is the single most important element to focus on to bring clarity to a buyer’s search. This figure should direct the price range for a buyer, which will determine which location, condition/features, and property type they can afford.

As you can see from the example of the Triangle of Buyer Clarity, buyers often have to adapt their search to meet their budget needs; it is rarely the perfect balance of an equilateral triangle. That could mean adapting by buying a townhome instead of a single-family home, going to a location that is a little further out, or being OK with a 90’s kitchen instead of a perfectly modern masterpiece. Getting into the market is more important than finding the perfect fit. The good news is that market trends show that townhomes, all locations throughout each county, and even 90’s kitchens appreciate! One could even tap into their equity down the road once it is built up and remodel that 90’s kitchen.Homeownership provides many benefits. Wealth-building opportunities are huge because we all need a place to live, so why not pay your own mortgage and gain appreciation instead of building your landlord’s portfolio? There are tax benefits, too, as you can use the interest as a write-off. Plus, you get the freedom to make your house your own and build a community where you live. You can paint the walls and dig in the dirt, and you don’t have to answer to your landlord. Overall, homeownership provides stability, freedom, and community. Helping my clients gain tangible and intangible benefits is the primary goal I work towards.

This is why I couldn’t let 2024 end without giving a shout-out to the would-be first-time homebuyers out there. My best piece of advice if you are considering buying your first home is to come up with a plan. I offer all of my clients a buyer consultation meeting where we review the market trends, apply their goals and search criteria, get them connected with a reputable lender, and devise a custom plan for them. The plan could start right away or sometime in the future; what matters is working towards the goal.

My mission is to help people gain the benefits of homeownership when they are ready. When I hand off the keys to a first-time homebuyer, it is one of the most rewarding aspects of my job because I know we have changed their lives for the better. If you are a potential first-time buyer or know someone who is, please reach out, I’d be honored to help.

If you’re looking for a new home, you might notice something called the ” Walk Score®” on property listings. But what does it really mean for you?

The Walk Score® algorithm calculates a score of walkability based on distance to 13 categories of amenities (e.g., grocery stores, coffee shops, restaurants, bars, movie theaters, schools, parks, libraries, book stores, fitness centers, drug stores, hardware stores, clothing/music stores). A high walk score means your new home is within walking distance to essential amenities—making life more convenient and car-lite!

What are the scores? 90-100: Walker’s Paradise.Daily errands do not require a car. 70-89: Very Walkable.Most errands can be accomplished on foot. 50-69: Somewhat Walkable.Some errands can be accomplished on foot. 25-49 Car Dependent.Most errands require a car. 0-24: Car-Dependent. Almost all errands require a car.

Curious about finding a home in a walkable area? Let’s explore together!

Your home is your shelter where you make memories, a large part of your financial nest egg, and a vehicle for creating wealth. Knowing what your home is worth is empowering and important. The reasons that may come up when you need to know your home’s value can have a direct impact on your financial health. Do you need to update your insurance, do some estate, tax, or financial planning, prepare for a re-finance, line of credit, or remodel, or are you considering a move? Relying on accurate home valuations for all of these endeavors will result in the best outcome.

To estimate your home’s value, you can easily jump on a public website that will spit out a value. This is called an AVM (Automated Valuation Model). There are a handful of free ones such as Zillow, Redfin, and RealEstimate. These sites are free for the consumer to visit and are based on a unique AI-generated algorithm that is typically a recipe of tax assessment data, CPI figures, market trend data, computer-picked comparable properties, and user-submitted data. They do not take into consideration important value points such as the condition of your home, improvements you’ve made, or nuances of the neighborhood; factors that only an actual person can evaluate.

It is important to note that on all three of these free sites, the algorithm and AVM tool are funded by the advertisers on the site, which are real estate brokers and lenders who want your business. The AVM is the carrot to get you in front of these high-paying advertisers who hope you click to connect so they can convert you into their real estate client. This is unlike the relationship-based business that I foster; this is more of a “sales-y,” transactional approach. Despite the sharks in the water, an AVM is a good starting point, like dipping your toe in the pool, but don’t get bit!

Here are the current AVM (Automated Valuation Model) values for a subject home from four sources (3 free and 1 fee-based). As you can see, the values vary. If you have a need to know the value of your home, don’t rely on an algorithm. According to Zillow, their accuracy varies by 7.49%; that is a huge variation! For example, that is $75,000, either high or low, for a $1M home. Depending on what you are planning for, that inaccuracy can severely cost you.

The AVMs above vary by 58%. If you apply the average Zillow accuracy percentage, the Zestimate® above could be off by $143,000 or more. It is important in this new world of AI that we do not underestimate the power of the human algorithm. Evaluating a home with all 5 senses, experience, and expertise is critical in establishing a home’s true value. Just like AVMs that vary, it matters who you align with, too. Hungry sharks who are paying to find clients, brokers who sell real estate as a hobby or side hustle, or brokers who are not engaged can all be detrimental. Seek out a professional who is committed to their craft, a student of the market, and up-to-date on market trends when you are assessing your largest asset.

If you want more precise information, consult a trusted advisor like me. By selecting accurate, comparable properties and analyzing today’s market trends, I will provide you with a much more comprehensive evaluation of your home’s value relative to its specific features, condition, and location. Please reach out if you are interested in having me tour your home and complete a Comparative Market Analysis (CMA) so you can plan for your future with confidence.

From saunas to gyms, more people are prioritizing private, custom spaces in their homes where they can focus on routine without distraction.

Saunas & Steam Showers

A steam shower is typically a stand-alone shower stall that can produce steam without running the hot water. The shower enclosure is sealed off from the rest of the bathroom, creating a self-contained humid environment that can also be used for bathing.

A steam shower is similar to a sauna in that it promotes relaxation with heat, but these two amenities require different equipment. A sauna—even a wet sauna—begins with dry heat from a stove or rocks. Users can choose to add some humidity with steam, but it rarely passes 60%, whereas steam showers provide close to 100% humidity. Saunas also aren’t equipped to handle running water like steam showers are. Saunas get substantially hotter than steam showers do, but because steam inhibits your sweat response, steam showers will allow you feel the effects of the heat more quickly and intensely than the sauna.

A home steam shower costs about as much to install as a home sauna. Both provide similar health and relaxation benefits, though steam offers more relief for dry skin and respiratory issues. If you’re considering including a sauna or steam shower as part of a bathroom remodel, the difference may come down to personal preference and available space.

Home Gyms & Studios

Your home’s design should include more than just your personal style; it also should accommodate your hobbies and lifestyle. If you’re committed to keeping active and working out regularly, a home gym might be a necessary part of the floor plan. Being able to fit a workout in when you have the spare time during the day without having to run across town can be life-changing.

Even better is a space that is beautiful and well thought out. A functional and aesthetic space can be welcoming and energizing. Start by bringing your own personal style into the space. Maybe a rattan light fixture or a fun wallpaper. If you don’t have room for a lot of equipment, opt for pieces that are designed to be easily stored out of the way, like a walking pad that can be folded and hung on the wall instead of a full stationary treadmill. Protect your floors from damage with rubber mats. They will also help to reduce the noise of the equipment, especially if you’re on the second floor of your home.

Wellness & Hobby Spaces

Wellness rooms can be about physical wellness, of course, but they’re also about mental well-being and can encompass anything that makes you feel calm, centered, connected, and rejuvenated. More people are realizing the importance of prioritizing their physical AND mental health. A wellness space can be for many different things: a music room, meditation, library, or even a dedicated space for hobbies. Think about what your goals are before designing your retreat.

Even a small nook exclusively devoted to your wellness space can be beneficial. No matter the size of your space, start with some basic elements and then build from there with things that bring you calm and happiness.

• Add sounds of nature or aromatherapy to lift your mood

• Choose nature’s colors for your eyes to land on, such as blues, greens, and neutrals

• Clear away any distractions

• Surround yourself with plants on the ground, table surface, and hanging

• Make your space comfortable with a cozy throw

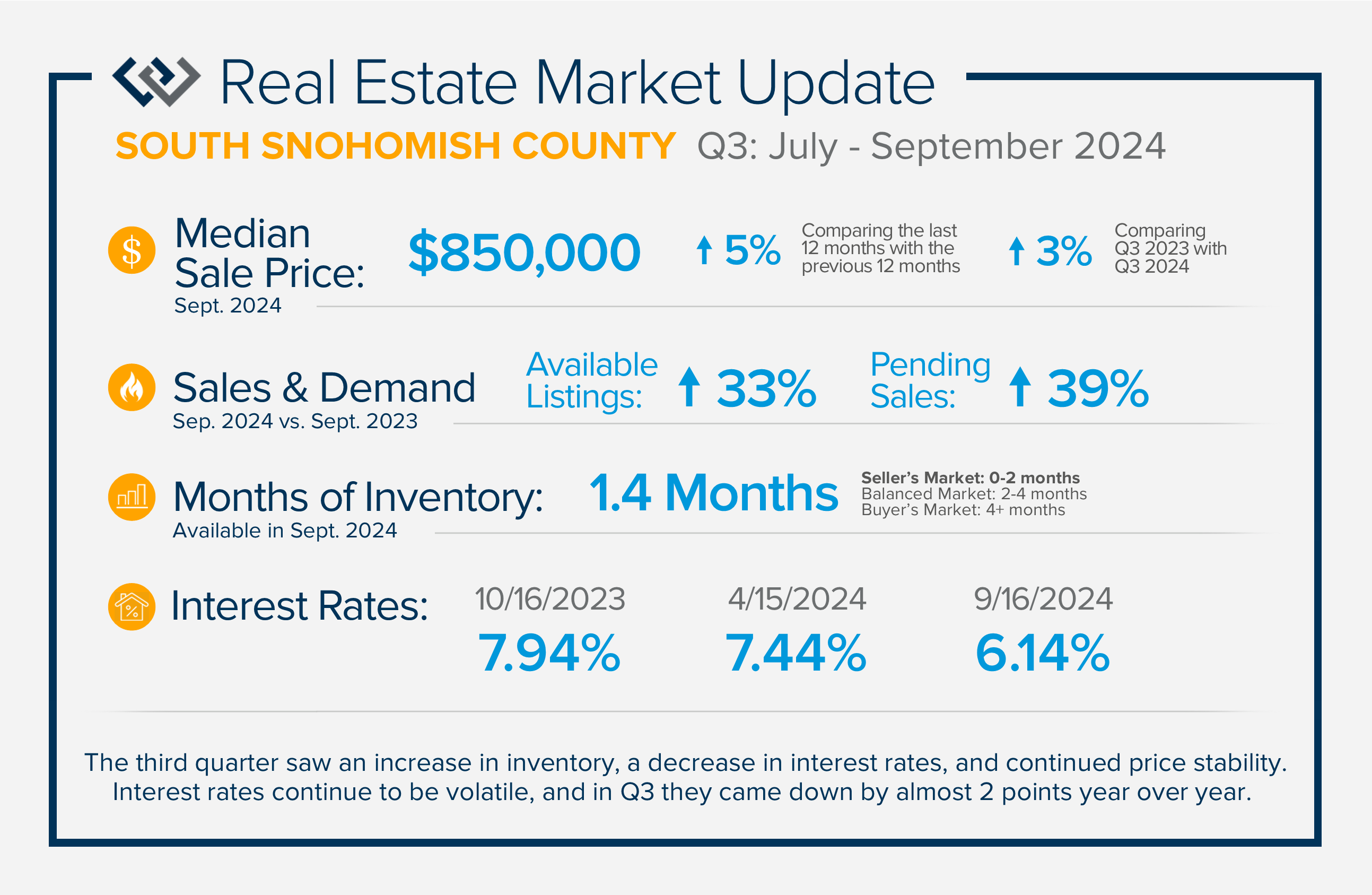

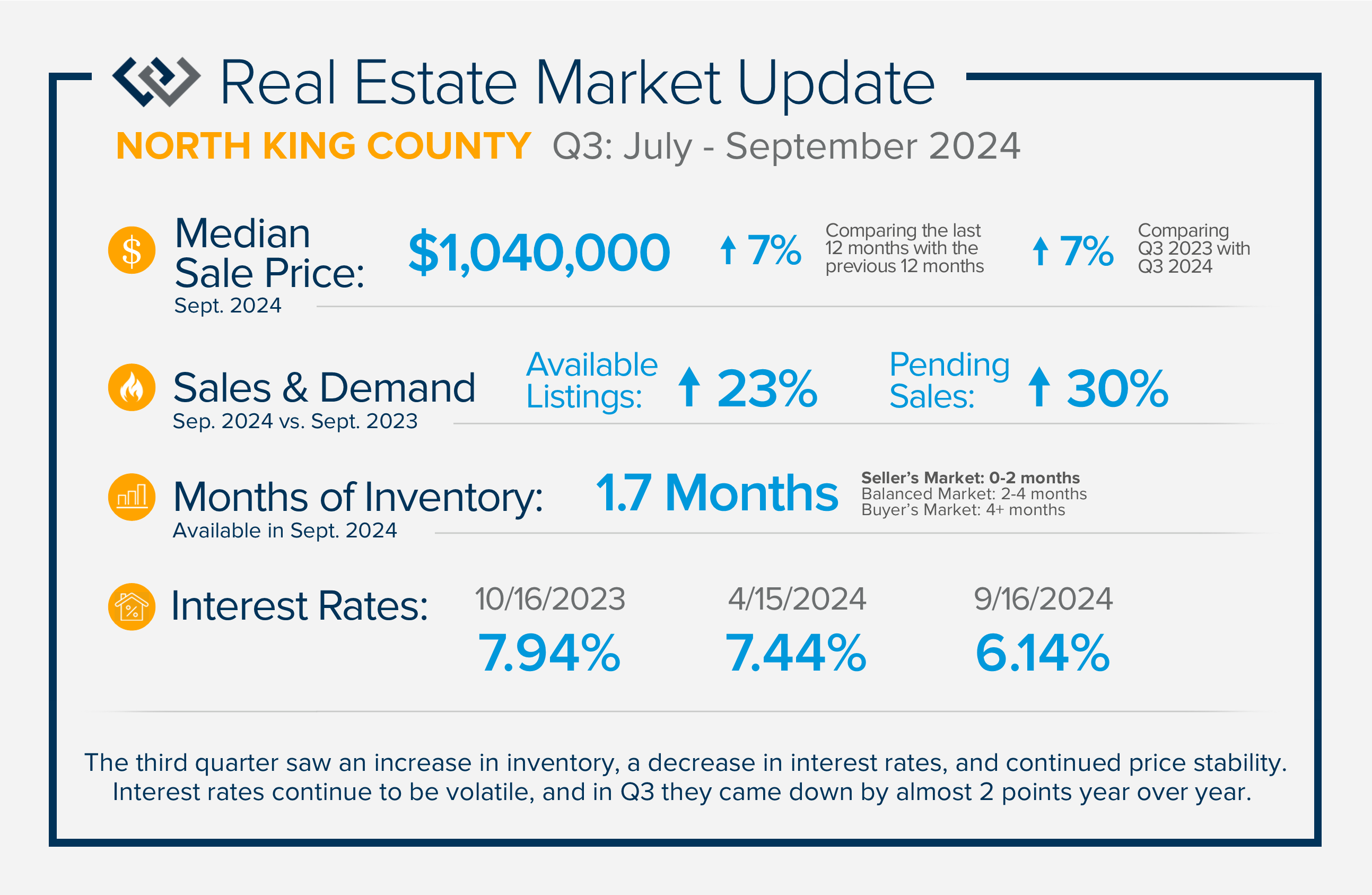

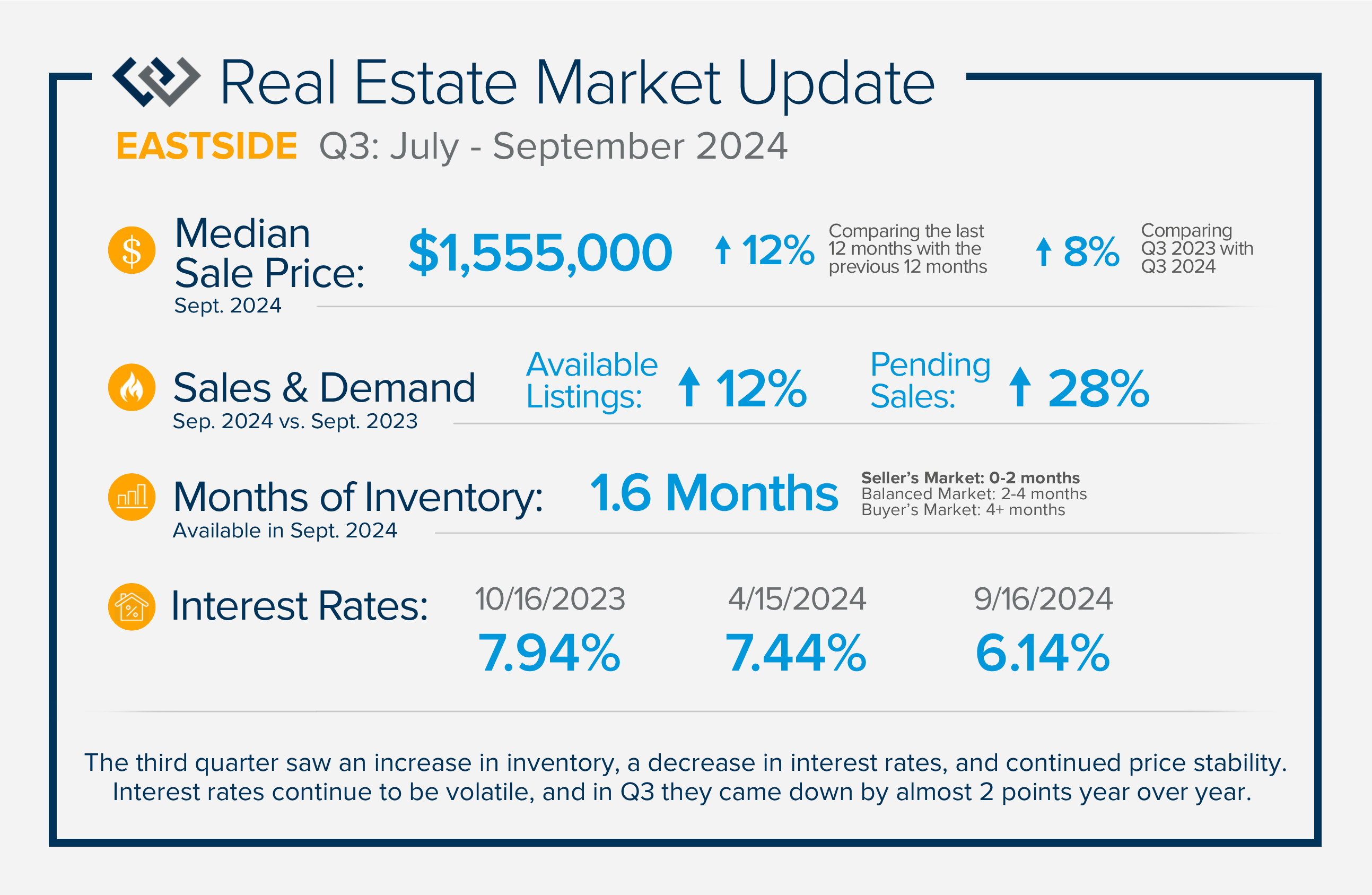

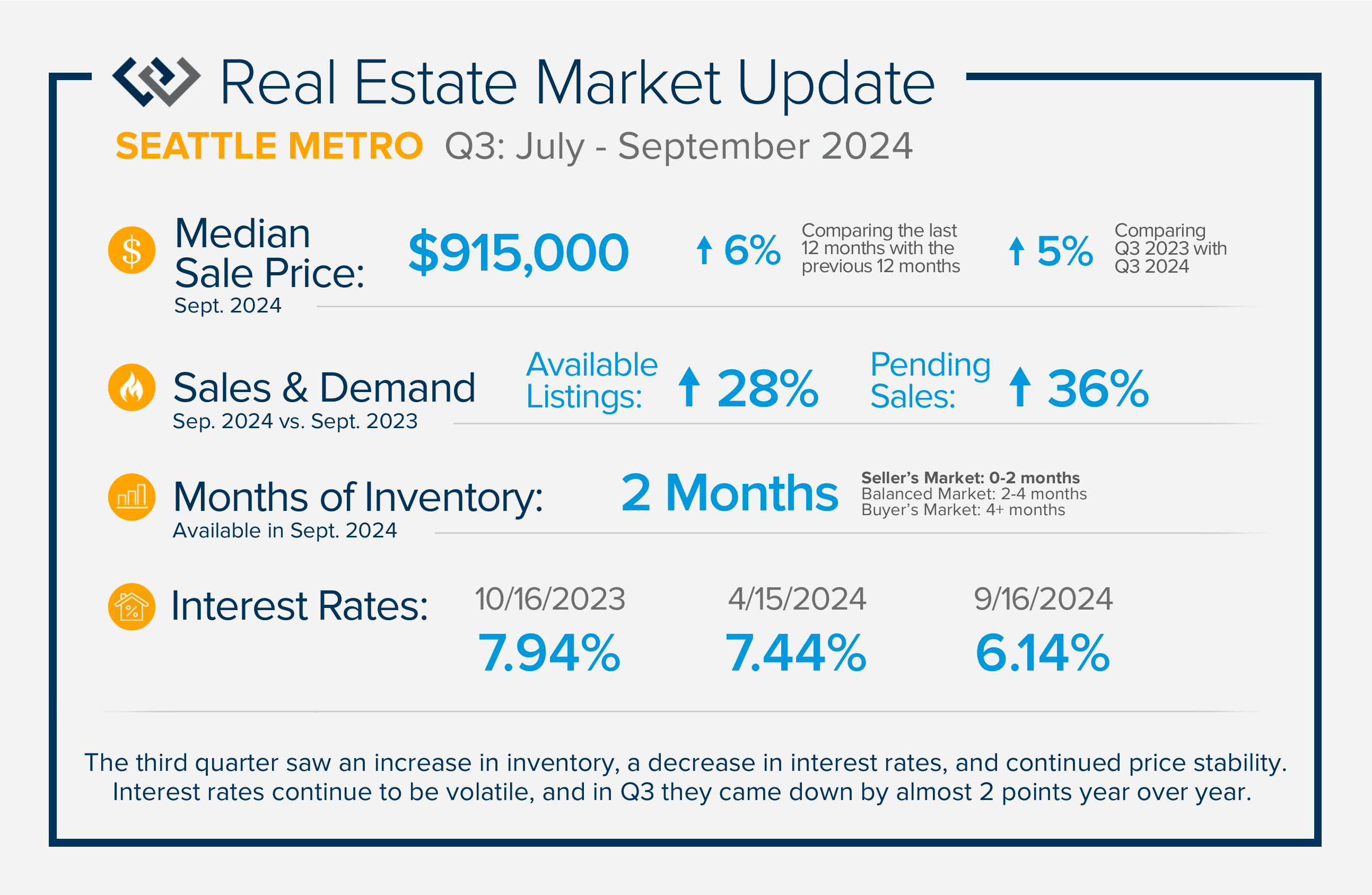

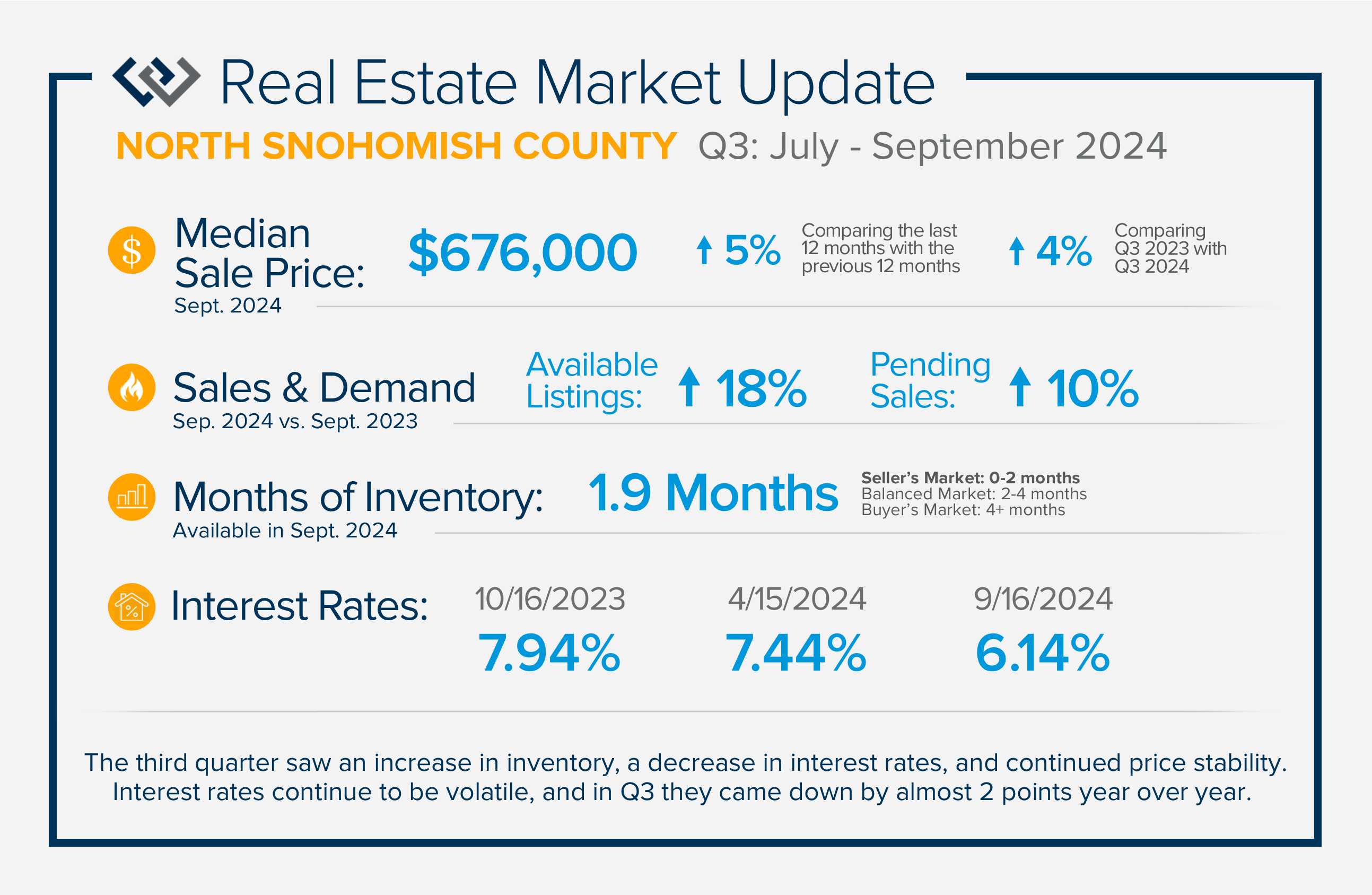

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

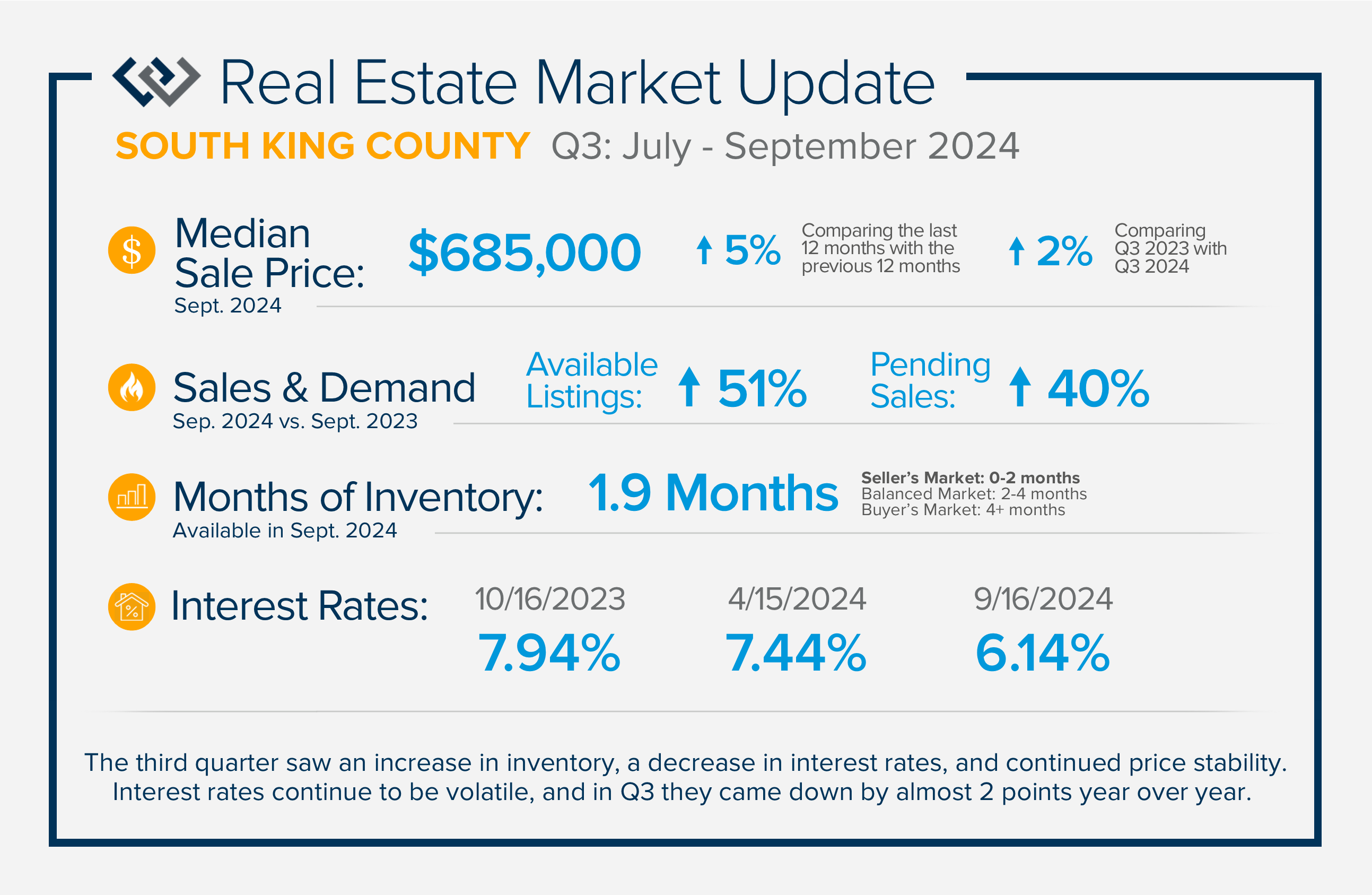

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

The third quarter saw an increase in inventory, a decrease in interest rates, and continued price stability. Interest rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

If you are curious about how market conditions affect you, please reach out. I aim to educate my clients to empower strong decisions.

As we celebrate the start of autumn, the season of change, the leaves on the trees are not the only things that are falling. Interest rates have gradually fallen throughout the year. Just 11 months ago, rates were almost 2 points higher; in the frothy spring market, they were nearly 1.5 points higher. During this same time, the median price in King County and Snohomish County grew. In King County, the median price was recorded at $975,000 this August and at $775,000 in Snohomish County, which are both up 7% year-over-year from August 2023.

Another trend that we are witnessing is a rise in available inventory for sale. August recorded the highest level of available homes for sale since the fall of 2022, two years ago. There were 3,105 available homes for sale in King County in August 2024 compared to 1,207 in January 2024, and 1,147 in Snohomish County in August 2024 compared to 374 in January 2024.

The combination of lower borrowing costs and more selection should be a welcome change for buyers. When the inventory was much tighter in the first half of 2024 and interest rates were higher, prices were increasing at a rapid rate. We are starting to see new buyers enter the market and some who have sidelined themselves return. This indicates that prices will remain stable as we finish out 2024.

Currently, buyers have more selection and the opportunity to grab a lower monthly payment. As you can see from the chart below, buyers have a significant opportunity to afford a higher price point at a lower rate or stay at the same price point and have a lower monthly payment. The reduction in rate over the last year is reducing monthly payments and creating great long-term savings over the life of the loan. The rule of thumb for affordability is a 1-point shift in rate affects a buyer’s buying power by 10%. For example, a home priced at $800,000 with a 7% interest rate will have a similar monthly payment as a home at $880,000 with a 6% rate.

The hesitation I am seeing in the marketplace is a desire for rates to come down even further. The good news is that they are predicted to continue this gradual decline. Where I am concerned is a decrease in selection. If we look at seasonality, it is common for inventory to be low in the first half of the year, especially in Q1 (see the King & Snohomish graphs above). If rates continue their slide and fewer new listings come to market, buyers will find themselves duking it out in 2025. Right now, while there are multiple offers on some properties, there are more properties that are being negotiated into contracts with one buyer.

This has created a more nimble market, particularly for buyers who also have to sell their homes to reposition their equity into a downpayment. While tight inventory provides great leverage for a seller, many sellers are also buyers. Analyzing the market conditions to align the environmental influences to create the best possible outcome for your goals is paramount, and it will not be the same for everyone. Depending on my client’s goals, timing can vary.

Oh, and another sentiment I often hear is, “Will rates under 5% ever be back?” That is rather unlikely and will go down as a historic time in our economy. With that said, if you are in your “forever home” and you captured a historically low rate, kudos to you! Truly, so awesome! If you are not in the home that is right for you, now may be the time to curate a plan to get you into your next home. If homes were selling at a rapid rate and prices were appreciating this last spring with 10% less buyer power, I imagine next spring will be much of the same, if not more.

One final item to note is the election. History shows that post-election year markets are brisk with sales and experience price growth and rate decreases. I am paying attention to key indicators such as inflation figures, unemployment measurements, the gap between the 10-year treasury yield and mortgage rates, and our local market conditions in order to provide my clients with the most accurate and up-to-date information to empower strong decisions.

Are you curious how all of this affects you? Real estate is the number one tool for building wealth, and you also get to live there. I think that is pretty important, and I love nothing more than providing valuable insights, having strategic conversations, and helping people align their homes with their lives. Home is where the heart is and also where your nest egg has the most reliable long-term growth. Please reach out if you’d like to dig into the details and apply them to your housing and investment goals.

Summer 2024 welcomed an increase in available inventory, a drop in interest rates, and continued price stability, which has upheld strong home equity levels. After a double-digit ramp-up in price appreciation in the first half of 2024, prices have slightly come off the peak of May 2024 and found stability. This trend is historically consistent with seasonal patterns and nothing to be alarmed about.

Increased selection for buyers was a welcome relief as inventory was extremely tight in the spring. While there are still homes getting multiple offers and escalating, we have also seen some buyers make purchases contingent on the sale of their current home. The market has become a bit more nimble for buyer’s terms in some cases. It is important to understand the nuances of each location, product, and price point, as the environment can vary which would indicate whether a buyer would need to compete or be able to negotiate more.

These trends are coupled with rates dropping below 7% in June and they have recently sat in the mid-6%. Rates were a point and a half higher in October 2023; this is a great improvement! We anticipate rates slowly dropping further which will put upward pressure on prices. The Fed meets again this month and if rates come down even more, buyer activity will increase. Between the lower rates and higher inventory, buyers should be excited and ready to act!

As you can see from the chart below, this shift in rate directly relates to a buyer’s monthly payment. Homes are expensive, so the cost to carry a loan is critical. These recent drops are helping out and should be paid close attention to as buyers are payment-driven in most cases. The opportunity to secure a home now with today’s rate could mean a buyer could enjoy a stable price and choose to re-finance or adjust to a lower rate later, keeping their same basis. Buyers should also understand that homeownership is a key component to building wealth.

I anticipate a healthy late summer and fall market. Over the Labor Day Weekend, buyer traffic was busy despite the holiday and activity is bubbling up. The lower rates are helping some folks jump off the fence. Even some sellers are getting ready to sell and relinquish their lower rate, so they can move to a home that better fits their needs. I’m excited about the real estate market for the remainder of 2024 and into 2025. If you are curious about how the trends relate to your goals, please reach out. I am committed to staying connected and up-to-date on the latest trends so my clients make well-informed decisions.

Here is a quick update on a topic I have been keeping you up-to-date on all year. On August 17, 2024, the NAR Settlement requirements were enacted. This required significant changes to real estate practices across the country. This made big news and stirred headlines. The good news is in WA state we made the majority of these changes back on January 1, 2024, when the law surrounding buyer agency was changed.

Since January 1, 2024, we have been required to obtain Buyer Brokerage Services Agreements (BBSAs) with buyers we are providing real estate brokerage services. These agreements can be exclusive or non-exclusive, must establish clear buyer brokerage compensation parameters, have a defined agreement term, and call out whether dual agency is allowed. I have embraced these changes and have brought value to my clients through this modernized process.

Our local MLS, the NWMLS, chose to opt out of the NAR settlement in May 2024. They felt confident that the risk for exposure was low due to advancements they have been making since 2019 to elevate transparency around brokerage compensation. Their proactive consumer-focused approach along with the new WA state law have had our state ahead of the curve.

The majority of the required practice changes required by the settlement were already in place in WA state as of January 1, 2024. Due to their choice to opt out, the NWMLS will not have to comply with the requirement to not publish a seller’s offer of compensation to a buyer’s brokerage. This is confusing to all parties of a transaction and the opposite of transparency. I am proud to run my business as a member of the progressive NWMLS and under the new law established by our state on January 1, 2024.

On August 15th, 2024, the NWMLS made some slight updates to some of their forms to coincide with the final settlement details. Most notably, buyer brokerage compensation was made more clear in the Purchase and Sale Agreement. It can be connected to what the seller is offering in their listing, what is agreed upon in the BBSA, or both. Sellers can choose to offer buyer brokerage compensation, choose not to, or request to negotiate it as a term in a buyer’s offer. Depending on how the established BBSA aligns with the Purchase and Sale Agreement, the buyer brokerage compensation will be paid by the seller, buyer, or a combination of both.

If you have any questions about the settlement and all of the changes we have navigated since 2019 until now, please reach out. I am committed to providing valuable services and clear communication to the buyers and sellers I serve. I understand that purchasing and selling real estate is one of the largest financial decisions a person ever makes and it is often related to big life changes. Navigating such importance takes great skill and care and I am committed to obtaining the best results for my clients while creating an enjoyable experience along the way.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $1,240 and 1,058 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

tes continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

tes continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

tes continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

tes continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

rates continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

es continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

es continue to be volatile, and in Q3 they came down by almost 2-points year-over-year. This caused more buyers to enter the market and pending sales to rise. The number of available listings has improved after a very tight start to the year. Some sellers have been willing to forego their previous low rates for a new house, creating more movement in the market. The combination of lower rates and more selection should have buyers excited to make a move. Equity levels remain strong in our region as prices have remained steady and appreciated year-over-year.

in the marketplace is a desire for rates to come down even further. The good news is that they are predicted to continue this gradual decline. Where I am concerned is a decrease in selection. If we look at seasonality, it is common for inventory to be low in the first half of the year, especially in Q1 (see the King & Snohomish graphs above). If rates continue their slide and fewer new listings come to market, buyers will find themselves duking it out in 2025. Right now, while there are multiple offers on some properties, there are more properties that are being negotiated into contracts with one buyer.

in the marketplace is a desire for rates to come down even further. The good news is that they are predicted to continue this gradual decline. Where I am concerned is a decrease in selection. If we look at seasonality, it is common for inventory to be low in the first half of the year, especially in Q1 (see the King & Snohomish graphs above). If rates continue their slide and fewer new listings come to market, buyers will find themselves duking it out in 2025. Right now, while there are multiple offers on some properties, there are more properties that are being negotiated into contracts with one buyer. election. History shows that post-election year markets are brisk with sales and experience price growth and rate decreases. I am paying attention to key indicators such as inflation figures, unemployment measurements, the gap between the 10-year treasury yield and mortgage rates, and our local market conditions in order to provide my clients with the most accurate and up-to-date information to empower strong decisions.

election. History shows that post-election year markets are brisk with sales and experience price growth and rate decreases. I am paying attention to key indicators such as inflation figures, unemployment measurements, the gap between the 10-year treasury yield and mortgage rates, and our local market conditions in order to provide my clients with the most accurate and up-to-date information to empower strong decisions.