The recently announced proposal of implementing a 50-year mortgage product had tongues wagging last week. There were countless articles, posts and news stories that jumped on the story. There was lots of debate about whether this type of product would be a smart choice in the long term, even though it provides a lower monthly payment. It is not a mystery that the biggest challenge in the real estate market is affordability, and that finding a way to lower monthly payments could help.

Bear in mind that this is speculative at this point, and would require policy changes that would take a year or more to complete if it is decided that this product will be brought forward. And of course, a trusted mortgage professional will provide the best insights; I have a curated list if you would like one. However, I thought it was important to discuss this as it relates to the affordability challenges we are facing in today’s real estate market. In addition, I see it as an opportunity to provide alternative solutions and highlight the benefits of homeownership. So here goes.

The median price for a single-family residential home in King County has increased by 39% since October 2020 and by 20% for condos. In Snohomish County, the median price for a single-family residential home has increased by 33% since October 2020 and by 42% for condos. This, coupled with higher interest rates, has caused monthly payments to jump up, sidelining some buyers.

For example, the median home price for a single-family residential home in Snohomish County in October 2020 was $570,000, and the interest rate for a 30-year fixed conventional loan was 3%, equaling a monthly principal and interest (P & I) payment of $1,922.51 based on a 20% down payment. Currently, the median home price in Snohomish County for a single-family residential home in October 2025 was $755,000, and the current rate for a 30-year fixed conventional loan is 6.25%, equaling a monthly P & I payment of $3,718.93 based on a 20% down payment. This comparison illustrates that monthly P & I payments have increased by 93% since 2020, almost double.

The good news is rates are down 1.66% from the 7.91% peak in October 2023 and down .75% from 7% since May of this year. That, along with decelerated price appreciation, has improved affordability, making now a better time than we have seen in the last two years to buy. The biggest obstacle is putting the historically low rates of the past that are not likely to return in the rearview mirror, and find other solutions to make a purchase. Perspective is key.

The 3-4% climb in rates since the pandemic heyday did not accompany a spiral in home prices. While median home prices peaked in mid-2022 as rates reached 5.5%, prices did correct but then moderated and stabilized. Year-to-date in 2025, prices have been unusually flat year-over-year in Snohomish County and up 1.4% in King County. It appears that home prices are holding and that any decrease in interest rate will only help maintain values and likely cause them to increase.

In fact, over long historical periods, many sources cite about 3% to 5% per year average appreciation nationwide. One estimate puts a long-term average appreciation at about 4.27% per year (1967-2024) nationally. More recently, over the past 5–10 years, some data shows average annual growth closer to 7%-9% due to especially strong market gains.

So, how would a 50-year mortgage help? Adding 20 more years of term to a loan will naturally lower the payment, but it increases interest payments and equity grows slower. Let’s use this example to help understand how it all pans out.

Let’s take a $750,000 home, with a 10% down payment and a conservative annual appreciation rate of 3%. Then apply an interest rate for a 30-year fixed at 6.25% and for a 50-year fixed at 6.5%. It is important to note that a longer mortgage term typically requires a higher interest rate. The 30-year product will result in a monthly P & I payment of $4,156, and the 50-year product will result in a monthly P & I payment of $3,805, a savings of $351 per month.

While lowering the monthly payment can be helpful to qualify for a higher loan amount and/or reduce monthly overhead, a borrower needs to consider their wealth-building strategy. In the first 10 years of the loan on a 30-year term, the borrower will pay $392,336 in interest and pay off $106,396 in principal; a total of $498,732 paid. On a 50-year term, the borrower will pay $431,546 in interest and pay off only $25,064 in principal; a total of $456,610.

Based on 3% annual price appreciation over those 10 years, the home’s value would be $1,008,000. The 30-year term borrower would have $439,396 in equity, and the 50-year term borrower would have $358,064 in equity, a $81,332 difference. Both options build more wealth vs. renting, which highlights the benefits of homeownership as one of the most powerful wealth building tools.

So, who should consider this option and who should not? And when I say consider, it doesn’t mean recommend – it means knowing your options. If this option were to show up in the future, most borrowers will review all their choices and then decide which product best suits their goals. Note, for many, waiting to qualify for a 30-year term may be a better choice given their circumstances and long-term plans.

Things to Consider With a 50-Year Mortgage

It can create a different balance between affordability and long-term cost. Here are some points to think about when deciding whether it might fit your situation:

Monthly Payment Flexibility

A longer loan term can reduce monthly payments, which may make a home feel more manageable from a month-to-month budget perspective. This can be helpful for buyers who want or need lower payments early on.

High-Cost Markets

In very expensive areas, stretching the term may make purchasing a home more attainable. It can be one way to navigate markets where prices rise faster than incomes.

Cash Flow Priorities

Some buyers prefer to keep monthly costs as low as possible so they can direct money toward:

Investments

Savings

Renovations

Other financial goals

A 50-year mortgage may support that flexibility.

Long-Term Plans for the Home

If you expect to stay in the home for a long time, the slower pace of equity building may feel acceptable in exchange for a lower monthly obligation.

Age & Income Trajectory

Younger buyers with many decades of earning ahead—or buyers anticipating future income growth—may feel comfortable taking on a longer-term loan with the idea of refinancing, selling, or paying extra over time. Although if you are able to pay extra, a 30-year loan makes more sense.

Other Factors to Keep in Mind

While there can be advantages, there are also trade-offs worth weighing:

Total interest costs will be significantly higher over the life of the loan.

Equity builds more slowly, which may matter if you plan to sell or refinance soon.

It may not fit well for buyers nearing retirement or those who want a rapid payoff timeline.

A 50-year mortgage can be one tool to improve affordability or cash flow, but it’s helpful to consider how the lower monthly payments align with your long-term financial goals, timeline, and comfort with the slower accumulation of equity.

Other options that can improve buyer affordability besides a 50-year term include some house hacking tricks. And the good news is these can be used now, given that the 50-year term is only a speculative, albeit one that got a lot of attention.

Some house hacking tricks that can help offset monthly payments include: buying a duplex or a triplex and living in one of the units and renting the other(s); buying with the plan to have a roommate(s) who will pay rent and offset your monthly payment; or buying with a trusted partner and sharing the monthly payment while you build equity together. In my next newsletter, during the week of Dec 8th, I will expand on these house hacking options, plus some others, and share some success stories.

Until then, the most important thing to understand is that owning real estate builds wealth faster than renting, but how long you plan to stay in the house and your loan term matters for the long-term equity picture. That is why it is important to consult with a trusted real estate professional and a skilled lender to help you organize and execute a winning, solvent plan.

As always, it is my goal to help educate and shed light on all of your options, so you are empowered to make strong decisions. If you or someone you know is curious about how today’s market trends align with your housing goals, please reach out.

November Home Maintenance 🏡✨

Prevent health and safety risks during cold months by updating the life-saving devices in your home with fresh batteries, evaluating the efficiency of your central heating system, and ensuring your plumbing is prepared for potential freezes as well as clear of blockages or leaks.

Cozy Kitchen: Creamy Chicken and Wild Rice Casserole Recipe

Looking for a cozy, crowd-pleasing dish to brighten up your week? This Chicken & Wild Rice Casserole is pure comfort—creamy, hearty, and perfect for chilly evenings or easy leftover lunches. It’s simple to prep, great for sharing, and guaranteed to bring a little homemade happiness to your table. Enjoy!

Ingredients:

2 cups cooked chicken (shredded)

1 cup wild rice blend (cooked)

1 can cream of mushroom soup

1 cup sour cream

1 cup shredded cheddar cheese

1 small onion (chopped)

1 cup mushrooms (sliced)

Salt & pepper to taste

Instructions:

Preheat oven to 350°F (175°C)

Sauté onions & mushrooms until soft.

Mix everything in a bowl, then pour into a greased dish.

As we round out 2025, I wanted to share some aspects of the current real estate market worth celebrating: equity and inventory! Below, you will see a 10-year equity study for Snohomish and King Counties, based on Single-Family Residential and Condos, along with a current assessment of inventory levels and their effects on the climate of the market. I felt it was important to bring you this information, whether you are a homeowner, renter, or if you are considering a move in the future. The market is finding balance, rates are gradually falling, and home values are maintaining.

Home equity is incredibly strong in our region and is the backbone of household wealth for many. This nest egg provides financial security, can be a vehicle to create a move to a home that is a better fit for your lifestyle, or provide the funds to do a home remodel. The long-term hold investment in real estate continues to be a bright light economically.

Inventory levels have increased over the last two years and we are experiencing balance in the market which is providing opportunities for buyers to strike with less rush and frenzy. This has been especially beneficial for those who need to sell their homes in order to make a purchase. We’ve started to see an uptick in contingent sales and bridge loans to make a move smoother and more attainable. First-time homebuyers are also seizing the opportunity to lock in a lower interest rate and the affordability of stabilizing prices. Rates have decreased by nearly 1 point since May 2025.

The image below from FHFA shows the long-term price growth (since 1991) in our state and metropolitan area. The figures are impressive at 480% in the state of Washington! I’d be happy to perform a custom equity study for you beyond the county information above and national figures below that is specific to your home’s specific features and today’s market trends.

Whether you own your home already or are considering building wealth through homeownership, I would love to help you analyze how equity growth and inventory levels could benefit your real estate goals. It’s always my goal to help keep you informed to empower strong financial decisions that augment your quality of life! Please reach out if you want to learn more.

🌶️ Cozy Kitchen: Tortilla Soup with Chicken & Avocado

Add a little Southwest flair to your fall table with this flavorful, comforting soup. Packed with tender chicken, fresh avocado, and a hint of spice, it’s a delicious way to warm up any evening.

Ingredients:

½ cup plus 2 TBSP vegetable oil

1 yellow onion

2 cloves garlic

¼ cup plus 2 tsp chopped fresh cilantro

1 cup drained canned plum tomatoes

½ tsp ground cumin

4 cups chicken stock

1 skinless, boneless whole chicken breast (about ½ lb) cut into bite-sized pieces

Salt & pepper

4 corn tortillas, preferably stale & dry

1 dried chile such as ancho, seeded

1 avocado, pitted, peeled, & diced

¼ cup shredded Monterey jack cheese

2 tsp fresh lime juice

Instructions:

In a frying pan over medium heat, warm 1 TBSP of the oil. Add the onion, garlic, and the 2 tsp cilantro and sauté just until golden brown, about 10 minutes.

In a blender or food processor, combine the sauteed mixture and the tomatoes and process until smooth.

In the same frying pan over medium-high heat, warm another 1 TBSP of the oil. Add the tomato mixture and cumin. Cook, stirring frequently, until thickened and darkened, 5-6 min.

Transfer the mixture to a large saucepan over medium-low heat and add the stock. Cover partially and simmer, stirring occasionally, until the soup is slightly thickened, about 20 minutes. Add the chicken and simmer until just opaque throughout, 2-3 minutes longer. Season to taste with salt & pepper.

While the soup is cooking, cut the tortillas in half and slice each half into thin strips. In a frying pan over medium-high heat, warm the ½ cup vegetable oil. Drop a tortilla strip in the oil, and if it sizzles immediately, the oil is ready. Drop handfuls of the tortilla strips into the oil and fry, turning with tongs, until crisp and browned, about 3 minutes. Using a slotted spoon, transfer to paper towels to drain.

In a small, dry frying pan over medium heat, toast the chile until fragrant, about 7 minutes. Shake the pan often; do not let the chile burn. Let cool, then crumble and set aside.

To serve, ladle to soup into warmed bowls. Divide the tortilla strips, crumbled chile, and ¼ cup cilantro, the avocado, cheese, and lime juice evenly among the bowls and serve immediately.

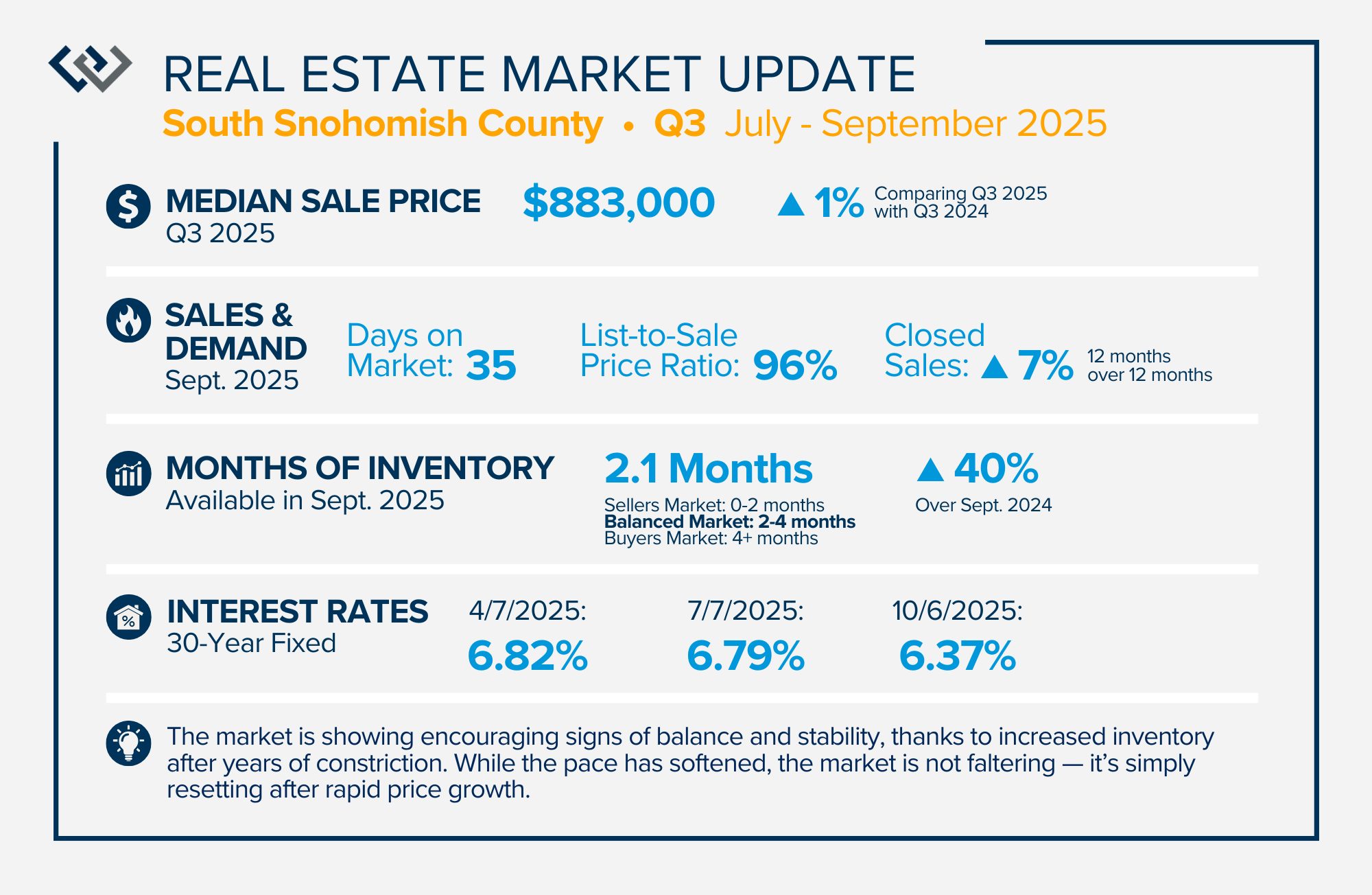

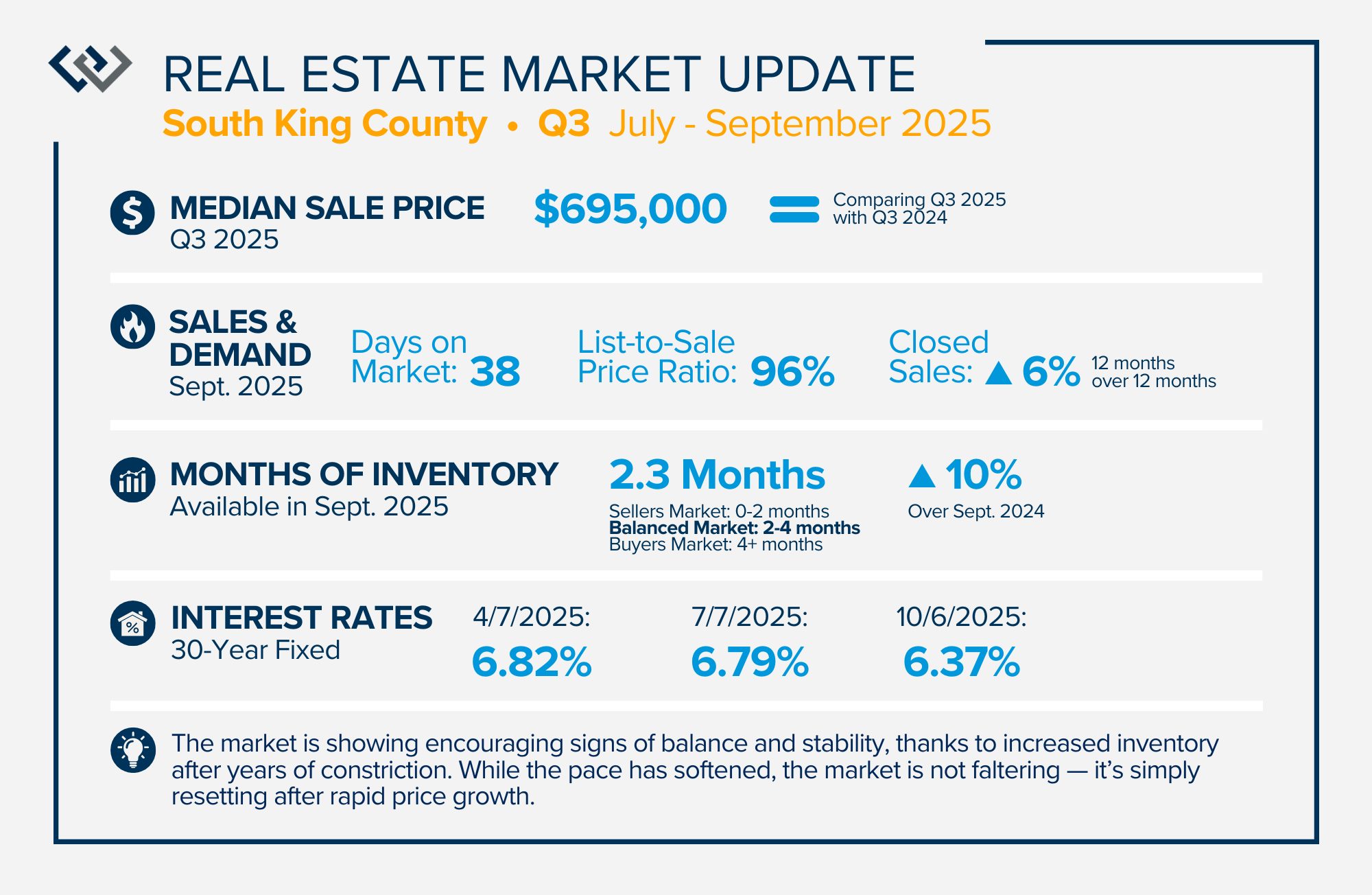

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

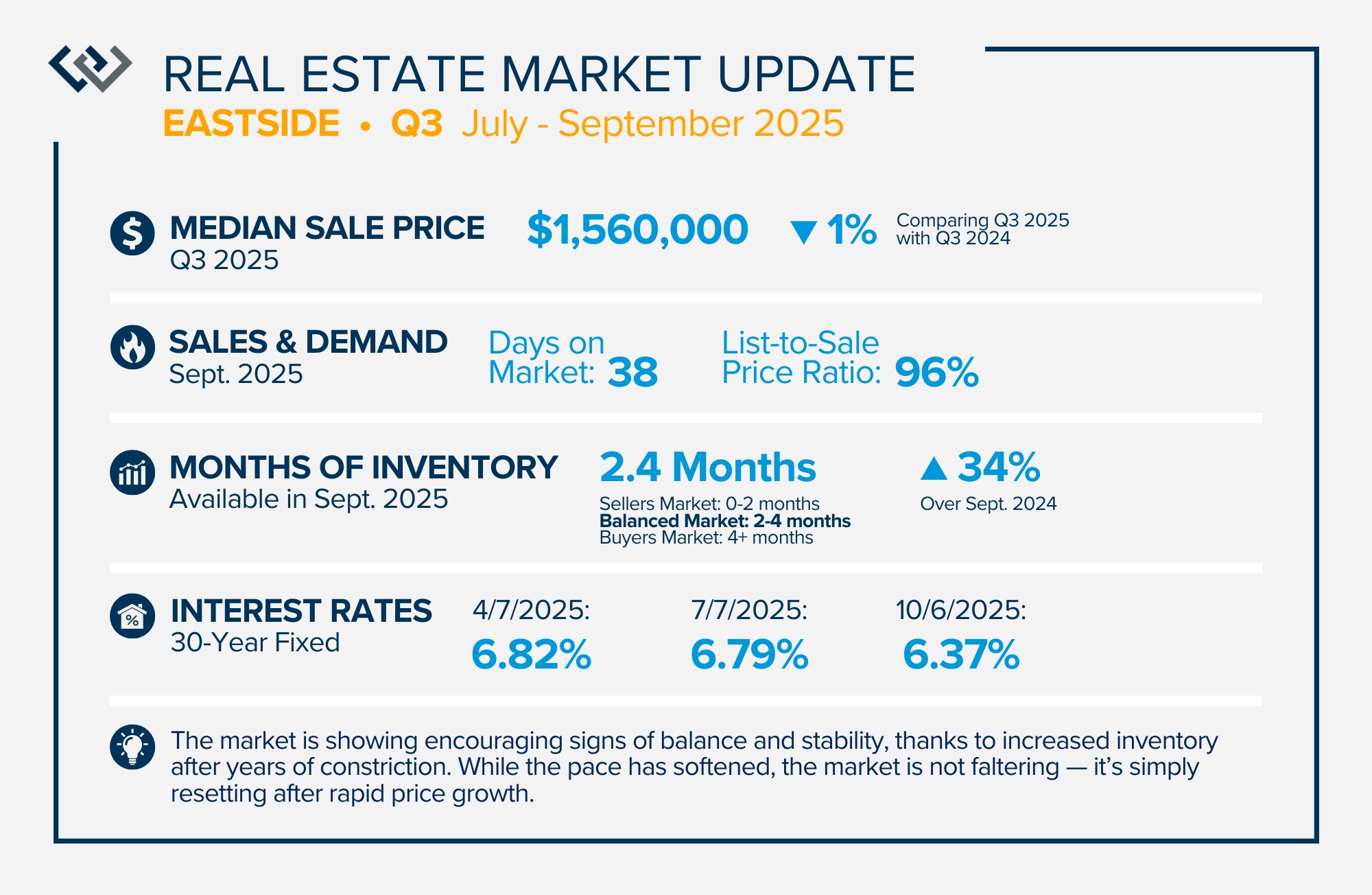

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

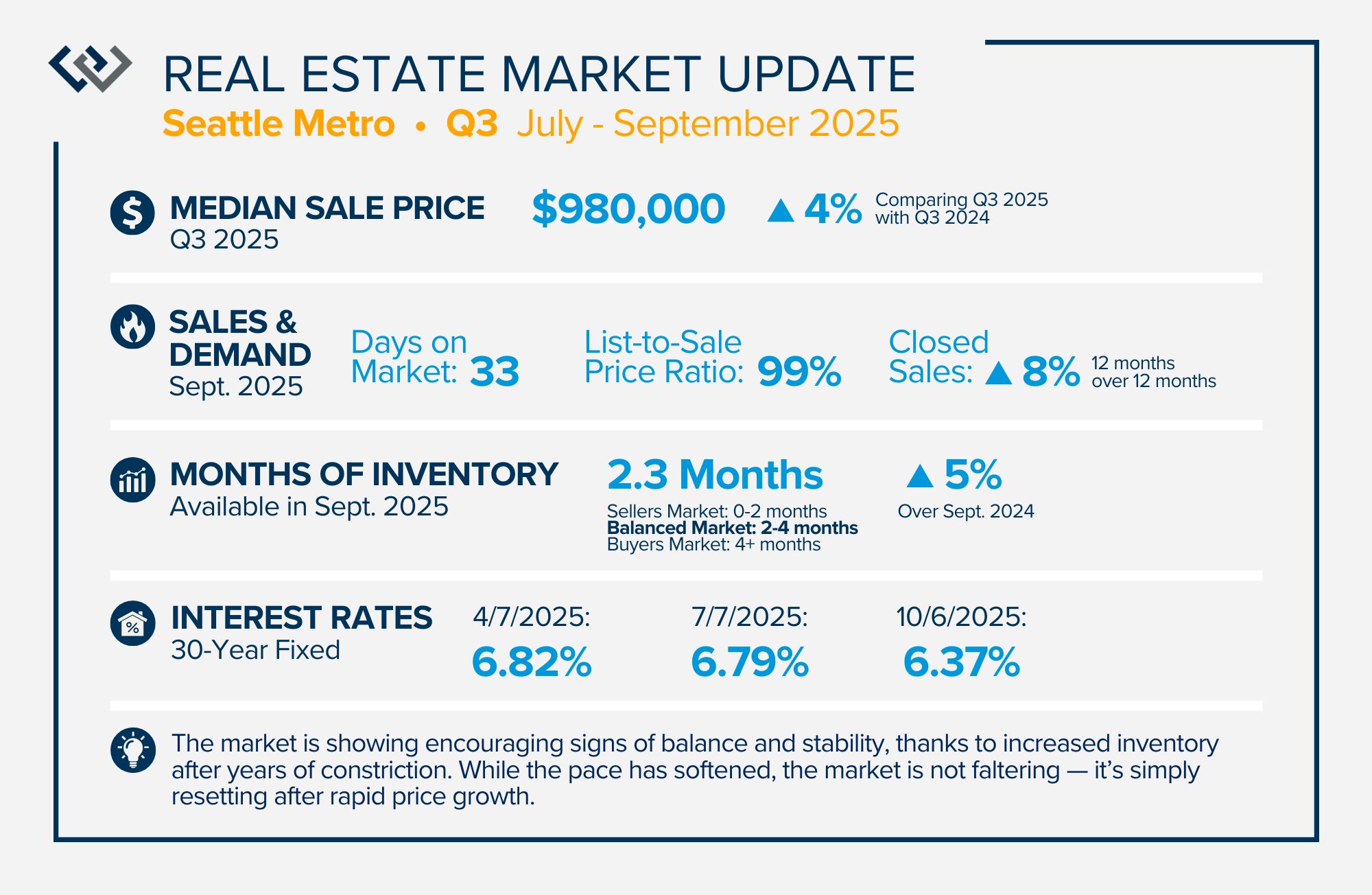

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

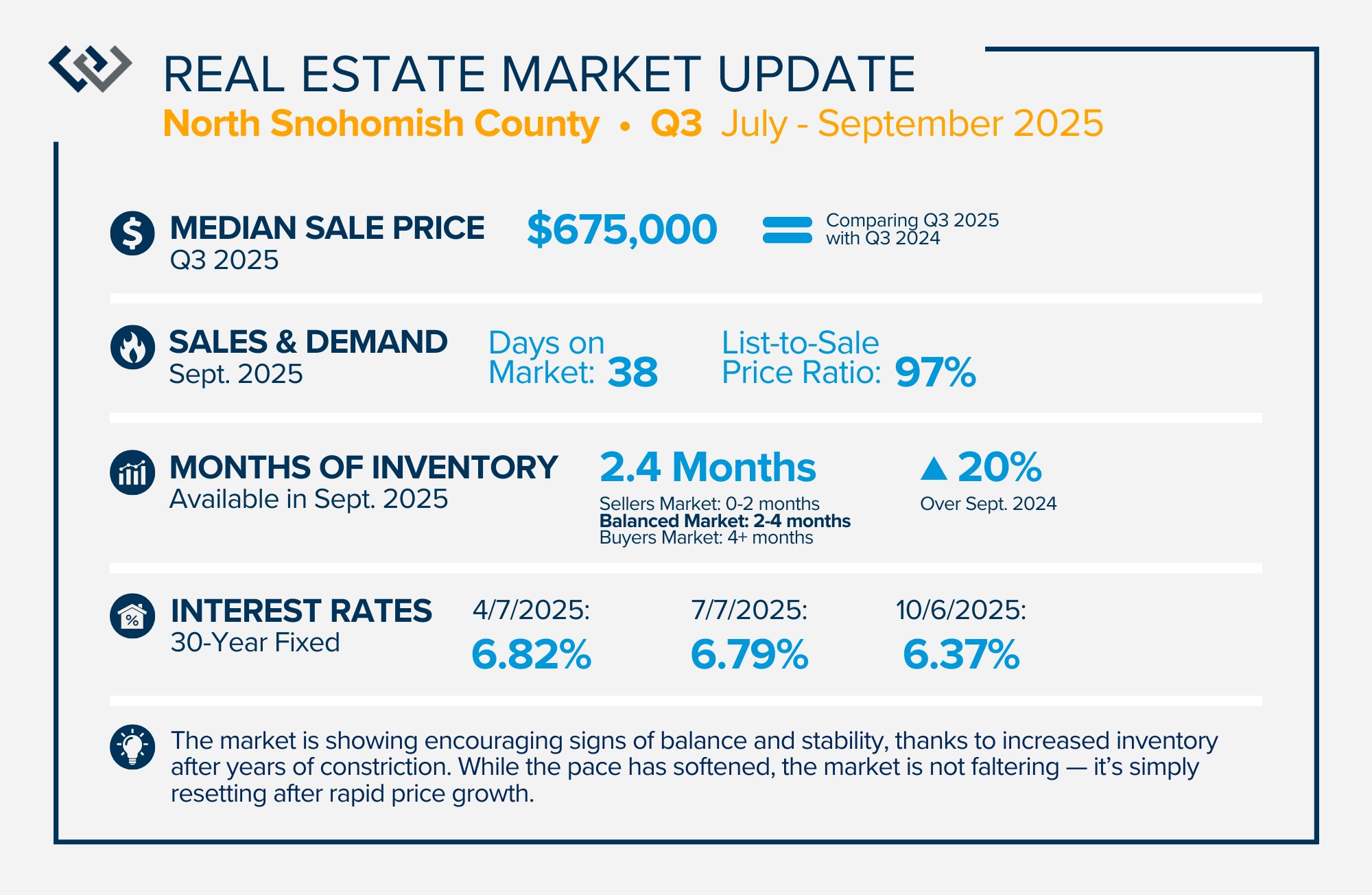

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

The numbers tell us we’re steady, not sinking. Let’s replace uncertainty with perspective and see how stability sets the stage for opportunity and long-term success.

After years of rapid appreciation, the market is simply taking a breath. Prices are holding steady, inventory is at its healthiest level in over a decade, and interest rates are easing — all signs of balance, not decline. If you’ve been feeling uncertain about the housing market lately, you’re not alone. The media (news or social) loves drama, but the data tells a quieter, steadier story. What we’re seeing right now isn’t a recession — it’s a reset.

The combination of rates coming down by 0.78% since January 2025 and prices remaining flat year-over-year means that monthly payments for a new mortgage are starting to ease. This is a welcome trend for buyers who have been grappling with affordability. We’ve even started to see buyers who already own a home, willing to give up their lower rate to make moves to homes that better fit their lifestyle needs.

Another reason we are not in a recession is the abundance of equity many homeowners have. Median price in King County is up 33% since 2020 and up 98% since 2015. In Snohomish County, the median price is up 42% since 2020 and up 115% since 2015. During this time, prices grew quickly vs. the historical norms of 3-5% a year. Hence, prices remaining flat makes sense as the market levels out and finds its equilibrium. Further, according to Census data, a record 40% of Americans own their homes free and clear, the highest level recorded.

This kind of “flat” market often feels uncomfortable because it’s different from the fast-paced, multiple-offer environment we grew used to and found exciting. But in reality, flat doesn’t mean failure. It means opportunity — for buyers to make thoughtful moves without frenzy, and for sellers to position their homes strategically in a more stable environment and reap their well-established equity.

In my years of watching market cycles here in the Greater Puget Sound Area, I’ve learned that perspective is everything. For sellers, how long they’ve been in their home, assessing their equity level, and where they want to go are what matters most. A segment of the market that I’ve seen take a step back is speculative sellers hoping to buck the current trends and make a quick gain.

It is important to note that owning real estate is a long-term hold investment and not an overnight come up. The extreme ramp-up in home values from 2020-2022 skewed that viewpoint for some. A valuable rule of thumb to adhere to is the 5-year rule. Outside of the Great Recession of 2007-2012, holding for 5 years has overcome a flat market or any short-term dips in values. It’s also important to understand that your home serves two purposes: your safe place and an investment.

A home is surely an investment, but also a place to call home. It doubles as the place where one finds shelter, makes memories, and becomes a nest egg over time. It’s impossible to “time” the market! It’s more so about matching your home to your current needs, affording the monthly payment, and planning to stay awhile. With those three elements in mind, a successful investment will happen along with living in a home that aligns with your life.

For buyers, we haven’t seen this calm of a market environment and selection in ages. In our region, we are currently experiencing a balanced market (2-4 months of inventory). In some areas of the country, a balanced market looks different (3-6 months), but for our area, it’s tighter due to density, industry, and limited land availability.

While we do occasionally still see multiple offers, they are no longer the norm. Buyers are now afforded the benefit of longer market times, allowing for negotiated contract terms to support performing due diligence over a longer time. They also do not have to escalate as high in price to obtain a home. My hope is that buyers who have sidelined themselves or are considering a purchase realize that this is a great time to buy!

If you’d like to talk about what this balanced market means for your goals — whether it’s buying, selling, both, or just planning ahead — I’m here to help you make decisions with confidence. Following the news, doomscrolling, or listening to an isolated story could veil you from the truth the data provides. While the market might seem “boring” right now, I’ve seen many buyers and sellers find great success. Let’s talk and apply your goals to today’s trends!

October Home Maintenance 🏡✨ Labor and building materials are typically the least expensive around this month, so utilize this to your advantage if you’ve been needing to make household updates or renovations to increase the marketability of your home. Prepare for the colder months by making sure your house is sealed from water damage and pests.

🍲 Cozy Kitchen: Hearty Chicken Noodle Soup

As the weather cools down, there’s nothing better than a bowl of homemade chicken soup. This comforting classic is easy to make, full of flavor, and perfect for cozy evenings at home.

Ingredients:

2 Tbsp vegetable oil

1 cup onion, chopped

3 garlic cloves, minced

10 cups chicken stock

1 tsp dried thyme, crumbled

¼ tsp dried dill

¼ tsp pepper

5 sprigs parsley

2 carrots, sliced

6 oz wide egg noodles

1 lb cooked chicken breast, cubed

2 Tbsp cornstarch

2 cups unflavored yogurt

¼ cup green onion, chopped

Instructions:

Heat the vegetable oil in a large pot over medium-low heat. Add the onion and sauté until soft, about 10 minutes. Add garlic and cook 2 minutes longer.

Stir in chicken stock, thyme, dill, pepper, parsley and carrots. Cover and bring to a boil. Reduce heat and simmer 20 minutes.

Remove and discard parsley, add noodles to stock. Simmer, uncovered, over medium-high heat until noodles are soft, about 10 minutes.

Add chicken and cover pot to keep soup hot. In a small bowl, stir cornstarch into yogurt, then combine with 1 cup hot broth. Return this mixture to soup pot and bring to a boil while stirring constantly.

Remove from heat and serve immediately, garnished with green onion.

Tip: This recipe makes enough to share. Drop off a bowl to a neighbor or freeze a batch for a busy weeknight.

From my kitchen to yours: wishing you warmth, comfort, and good company this fall!

Two unique opportunities have lined up for buyers: Lower Interest Rates – With rates down almost three-quarters of a point, a $500,000 mortgage costs $232 less per month than it would have just a short time ago. That’s nearly $84,000 saved over 30 years.

More Homes to Choose From – We’re seeing the highest inventory in 14 years, giving buyers more options, less competition, and greater negotiating power.

Why this makes it a good time to buy: Opportunity to Build Wealth – Prices are up 2% in King County and 1% in Snohomish County year-over-year and if rates continue to soften, prices will rise. Fixing your price now will lend itself to great, long-term equity growth. In fact, homes in King County are up 33% over the last 5 years and up 80% of the last 10 years. They are up 42% in Snohomish County of the last 5 years and up 98% over the last 10 years.

Find the house that best suits your life – Moves are brought on by life changes. If you see yourself entering a new chapter, whether it is joy-filled or challenging, a purchase can help align your home with your life. Pause to assess if now would be the right time to make a move and consider the advantages of the current market.

All of this means more affordability and more choices—a rare combination in real estate. Please reach out if you would like to learn more. It is my goal to help keep my clients informed so they are empowered to make strong decisions.

Making a move, whether it’s across town or across the country, can feel overwhelming. I understand that behind every “For Sale” sign there’s a personal story, and often, real-life challenges that make it hard to take the first step. Over the years, I’ve helped many clients work through these very obstacles, and I want you to know there are solutions for every situation.

Here are a few of the most common roadblocks I hear, and how we can overcome them together:

“My home has deferred maintenance or needs updates, but I want to sell for top dollar and don’t have extra funds.”

The Windermere Ready Loan is your “easy button” for accessing funds for listing prep. It allows you to access cash based on your home’s equity to cover cleaning, repairs, or remodeling—so you can sell faster and for more money, without having to pay upfront. The fees are low, access is fast, and we can devise a plan identifying which items will yield the greatest return. You can learn more about the program here or simply reach out to me.

“I’m overwhelmed by the amount of stuff I need to sort through before I can sell.”

You’re not alone in this. I work with trusted vendors who specialize in helping people clear, organize, and prepare their homes for the market. With the right team, what feels overwhelming becomes manageable. You’d be amazed at how this process can be freeing, uplifting, and empowering. Getting started is the hardest part, and I can connect you with great resources or simply help you devise a checklist that moves at your pace.

“I need to relocate, but I don’t know anyone in the new area. How do I find a good agent?”

That’s where my connections come in. With Windermere’s broad presence in the West and our global referral network through Leading Real Estate Companies of the World, I can introduce you to a great agent wherever you’re headed.

“I don’t have 20% to put down. Can I still buy a home?”

Yes, you can! The idea that you must have 20% down is a common misconception. There are loan programs available with much lower down payments—some as low as 3.5% and even 0%. I can connect you with excellent lenders who will walk you through your options.

“I can’t buy until I sell, but I don’t want to move twice.”

The Windermere Bridge Loan is one example of the various creative financing options that may be the perfect solution. It allows you to tap into your equity before your home sells, so you can purchase first and move only once. The process is designed to be simple, affordable, and stress-reducing. If the Windermere Bridge Loan is not the right fit, I have access to other lenders and programs that specialize in tapping equity to purchase before having to sell.

Let Practical and Caring Guidance Lead the Way

I’m in the business of solving problems and creating solutions that move people toward their next chapter in life. Home reflects life, and life is always evolving. Making a move can be deeply personal, and with the right guidance, it can also be a powerful step toward growth and improvement.

If challenges are standing in your way, please don’t keep them to yourself. Share them with me. I’ll listen carefully, and together we’ll create a plan that makes your move not only possible but successful.

Let’s Talk About Your Next Chapter

If you, or someone you know, are considering a move but feel stuck, I’d love to help. Reach out today, and let’s start a conversation about your goals. With experience, care, and trusted resources, I’ll guide you every step of the way so you can move forward with confidence and peace of mind.

September Home Maintenance 🏡✨ Before it’s time to turn on the heat, have your air and ventilation systems inspected by the professionals to ensure efficient and healthy airflow. Note: if you need to purchase or replace any major household appliances, September and October are usually when the latest models are revealed and are the best months to buy them.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

omes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

omes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

es to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

es to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

onstriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

onstriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

nstriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

nstriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

striction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

striction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

triction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

triction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.