Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Monthly Newsletter – 11/16/2023

|

|

over the next 12-18 months. In fact, we have seen rates drop half a point over the last 30 days. Currently, the 30-year conventional rate is hovering about 7.5%. We saw a correction in prices when rates jumped by a point and crested 6% in mid-2022. Since Dec 2022, prices found their bottom, and price appreciation started happening again. Year-to-date, the average interest rate has been around 7% and prices have not been in a free fall, they have grown and remain stable.

over the next 12-18 months. In fact, we have seen rates drop half a point over the last 30 days. Currently, the 30-year conventional rate is hovering about 7.5%. We saw a correction in prices when rates jumped by a point and crested 6% in mid-2022. Since Dec 2022, prices found their bottom, and price appreciation started happening again. Year-to-date, the average interest rate has been around 7% and prices have not been in a free fall, they have grown and remain stable. that happened in 2022, it is safe to say there is a correlation between prices and rates. If the experts are correct and rates fall over the course of the next year or so, we should anticipate prices to increase. That is what hangs in the balance when making the decision of whether to buy now or later. The example to the right shows the effect that price appreciation will have despite rates being lower. It was not that long ago that we were experiencing bidding wars where homes escalated in the double digits. As you can see, the higher price results in a higher payment even with the lower rate.

that happened in 2022, it is safe to say there is a correlation between prices and rates. If the experts are correct and rates fall over the course of the next year or so, we should anticipate prices to increase. That is what hangs in the balance when making the decision of whether to buy now or later. The example to the right shows the effect that price appreciation will have despite rates being lower. It was not that long ago that we were experiencing bidding wars where homes escalated in the double digits. As you can see, the higher price results in a higher payment even with the lower rate. If one is able to afford a purchase now with today’s rate, they can refinance when rates go down and save themselves a lot of money on their payment while keeping a fixed price. Additionally, if a buyer can secure a rate buydown, such as a 2-1 buydown, the higher rates can be overcome and a refinance can fix the rate when the rates drop.

If one is able to afford a purchase now with today’s rate, they can refinance when rates go down and save themselves a lot of money on their payment while keeping a fixed price. Additionally, if a buyer can secure a rate buydown, such as a 2-1 buydown, the higher rates can be overcome and a refinance can fix the rate when the rates drop. in monthly payment savings is paid upfront at closing and in some cases paid by the seller. The buyer still needs to qualify based on the 7.5% interest rate as the payments will convert to the payment based on the 7.5% in year three moving forward. The strategy here is to never have the payment increase to 7.5% because the buyer plans to refinance when rates come down, and will permanently fix their rate below 7.5%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases those funds can be applied towards the refinance.

in monthly payment savings is paid upfront at closing and in some cases paid by the seller. The buyer still needs to qualify based on the 7.5% interest rate as the payments will convert to the payment based on the 7.5% in year three moving forward. The strategy here is to never have the payment increase to 7.5% because the buyer plans to refinance when rates come down, and will permanently fix their rate below 7.5%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases those funds can be applied towards the refinance.|

|

|

|

Monthly Newsletter – 10/26/2023

|

|

|

|

South Snohomish County Market Report – Q3 2023

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative with interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

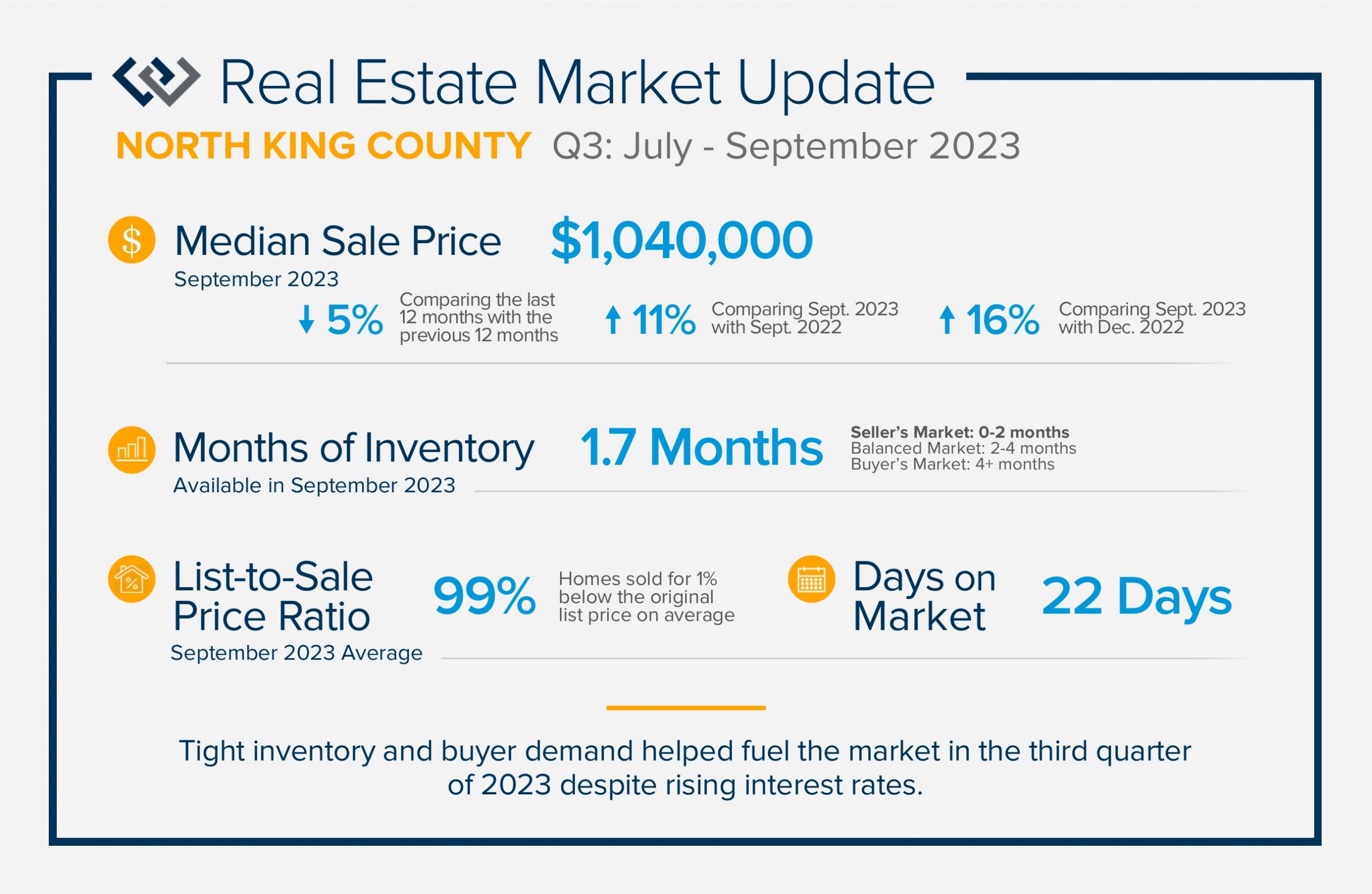

North King County Market Report – Q3 2023

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative with interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

with interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

Eastside Market Report – Q3 2023

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative wit h interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

h interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

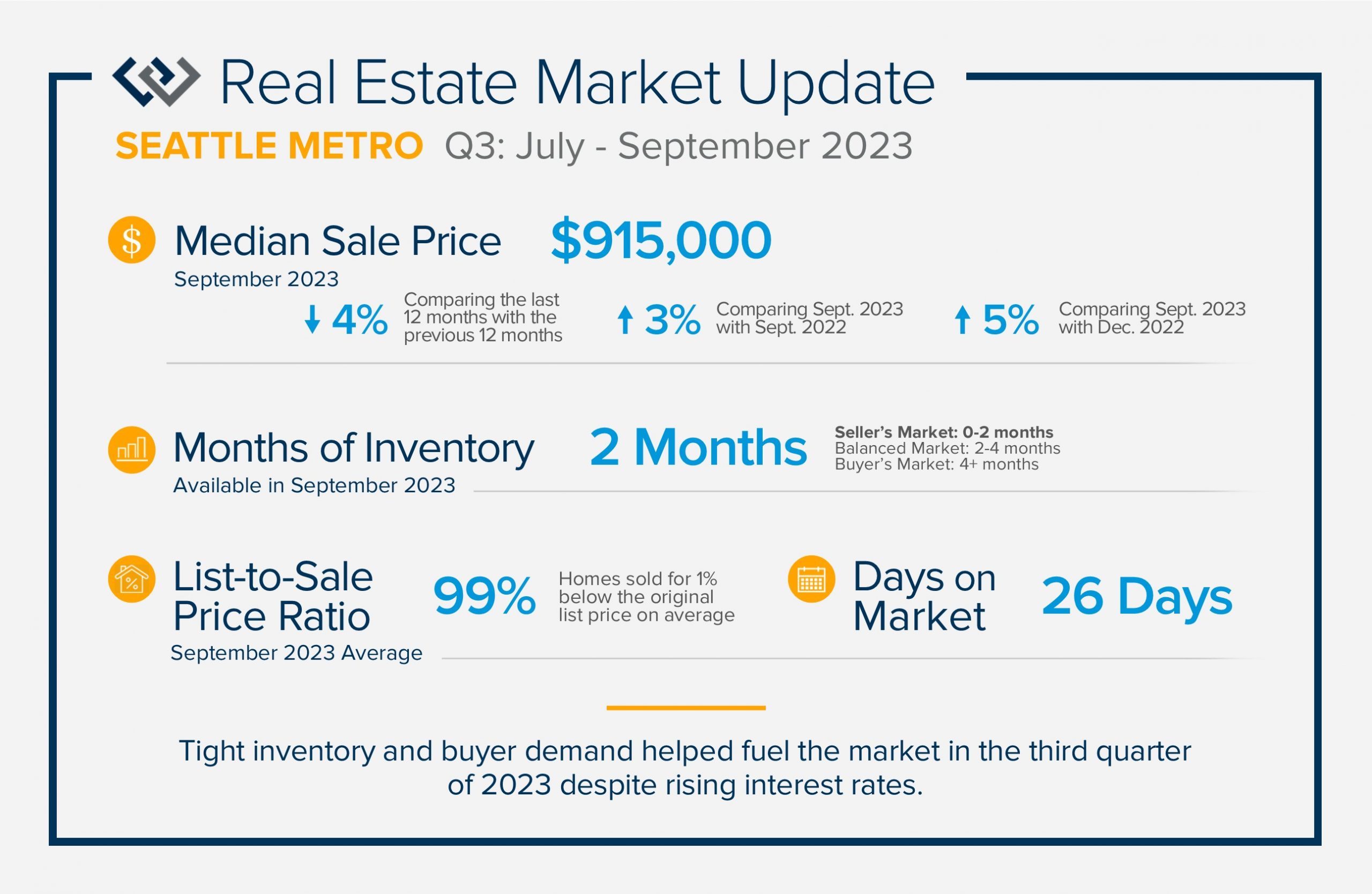

Seattle Metro Market Report – Q3 2023

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative with interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

North Snohomish County Market Report – Q3 2023

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative w ith interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

ith interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

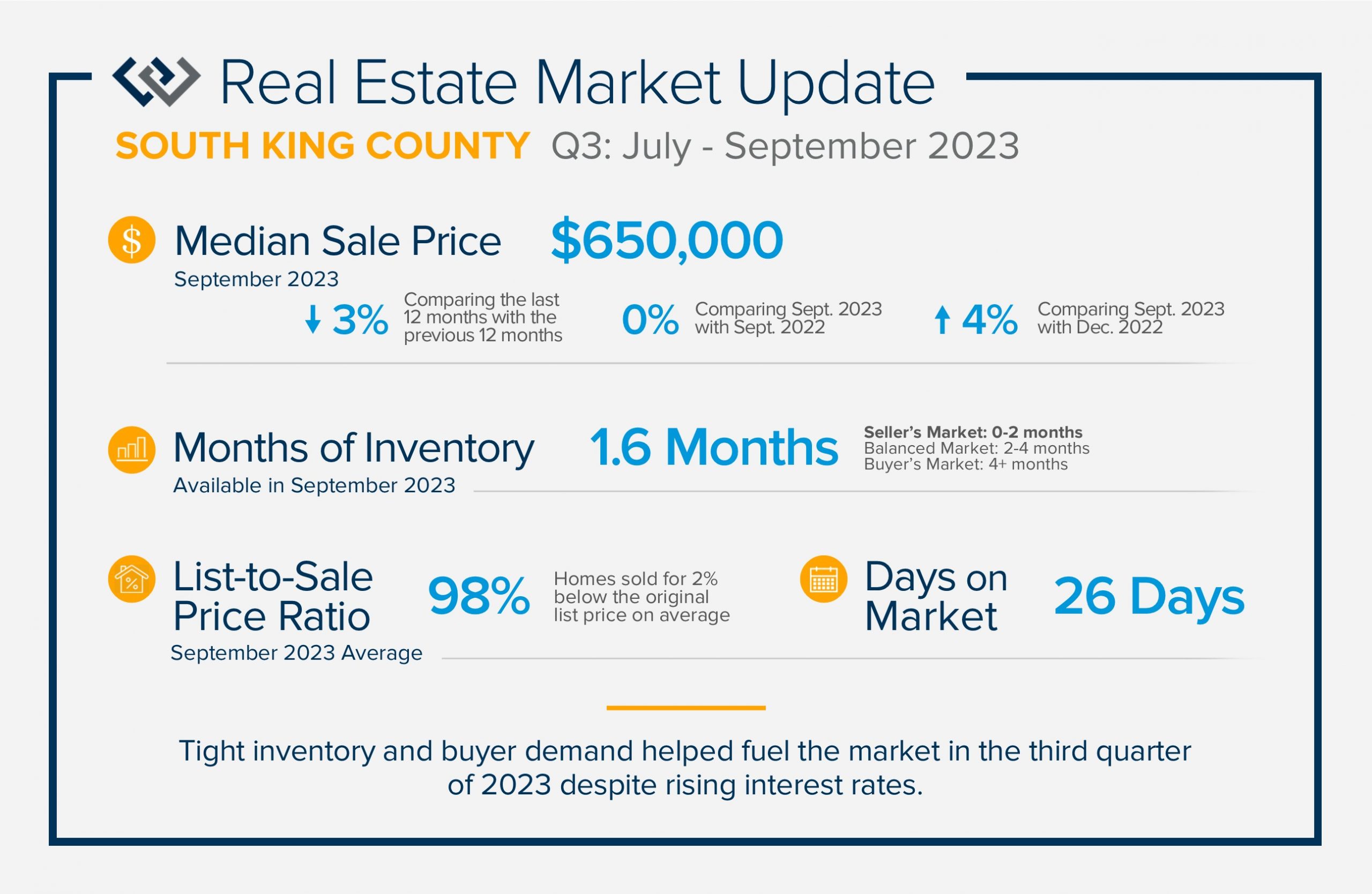

South King County Market Report – Q3 2023

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all  homeowners having 50% or more equity in their homes.

homeowners having 50% or more equity in their homes.

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative with interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

Monthly Newsletter 09/27/2023

|

|

|

|

|

|

|

Monthly Newsletter – 09/07/2023

|

|

a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens. shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.|

|

|

|

in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.|

|